As many of you may know, all of us are noticing a considerable increase in insurance rates this year. Not only that, but with firmer underwriting restrictions on driving records and property coverage, we would like to give you some guidance on surviving these current insurance trends.

Soft Market vs. Hard Market

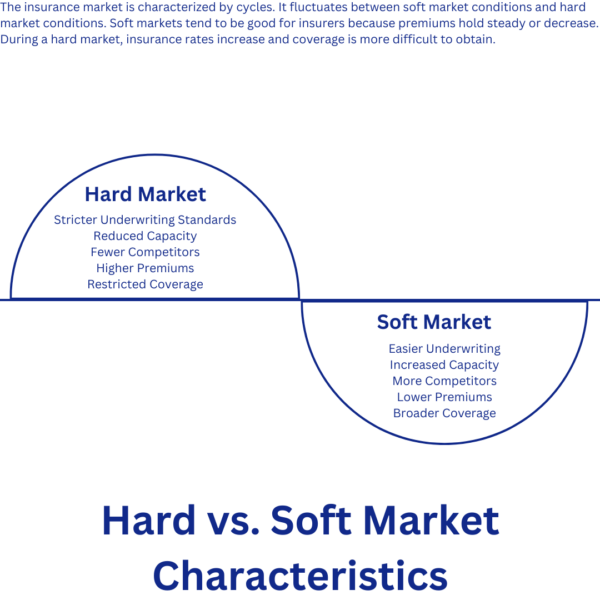

Like everything, the insurance market is cyclical. In a soft market, premiums hold steady or even decrease. Many insurance companies will lower their rates to try and grow. In a hard market, which we are experiencing right now, rates increase and coverage is harder to find because underwriting has gotten stricter.

Which market is best for shopping? At R.C. Keller & Company, we like to say “We will shop it around so you don’t have to.” In today’s hard market, we are telling our clients to “hunker down” in most situations and we have good reason why.

How Long Will This Last?

Historically, hard markets are shorter periods of time than soft markets. Our last hard market was from 2001 – 2004, whereas the latest soft market was 2004 – 2019. We have started to see our preferred carriers tighten up their underwriting guidelines, so a hard market is anticipated to last a bit longer. The historic inflation, combined with an increase in catastrophic weather events, has made insurance claims costly to resolve, 2022 saw record high losses for insurance carriers; which tells us the hard market is something we should get used to for awhile.

An Assortment of Restrictions

Below is a list of some underwriting restrictions we are seeing from our insurance carriers at the moment:

- Age of roof – some carriers will not write the business if your roof is over 15 years old.

- Overhanging trees – if branches are too close to the home, it can be flagged for non-renewal.

- Previous non-weather-related home claims will make a policy ineligible.

- Some carriers will require “bundled” business – auto + renters or auto+ home.

How to Make the Best of a Hard Market

The knowledgeable agents at R.C. Keller & Company love finding savings for clients. With these current insurance trends, moving your account to another carrier is unlikely the best option for your wallet. The last thing we would want to do is move a client who then gets hit with some unforeseen underwriting restriction that will disrupt their life or finances. For instance, many insurance carriers are not accepting business if you own a Kia or Hyundai. The R.C. Keller & Company team of independent insurance agents are best equipped to help you navigate this time in the insurance market because we are aware of what each carrier is doing with new and existing business. We also have a wide array of skilled referral partners we can recommend for any kind of home maintenance you need done.

Survival Guide for “Hunkering Down”

- Update your roof: Replacing your roof that is 15 years old or older will help your home stay maintained, better protect you when severe weather strikes and adjust your home insurance premiums slightly.

- Adjust your deductibles: Consider raising your deductibles during this time, some insurance carriers are making this mandatory for renewal for current clients. Homeowners, raising your deductible from $1,000 to $2,500 can help reduce your premium. This also forces you to give extra consideration before filing a claim. As home values and inflation continue to rise rapidly, this is almost a necessary step.

- Consult your agent before filing a claim: Insurance carriers are cracking down on insureds using their policies to cash in on a new roof or other updates to their home or car. Contact your R.C. Keller & Company insurance advisor before taking action on filing a claim. They will know how many claims you already have and what your insurance carrier may do if you file another one.

- Meaningful home maintenance: Are trees touching your home? Do you have ivy growing on the façade of your house? Are your front steps crumbling? Insurance carriers do exterior inspections of all new business and if you really need to move carriers, they may decline coverage if they see your property in disrepair.

- Added Safety Measures: Several carriers provide discounts for added safety measures like a home alarm system or installing water sensors. Update your R.C. Keller & Company insurance advisor if you have added any security measures for your home.

R.C. Keller & Company is Here to Help

If you have any questions or concerns your R.C. Keller & Company insurance advisor is here to help. We are honored by all the clients who trust our professional advice and services. We have a deep understanding of current insurance trends. Our professional advice based on your needs is why you chose us instead of an impersonal national service center hotline.